A Dubai-based trading company closes its financial year with record revenue. The board is satisfied. Three months later, the CFO is explaining to the same board why cash reserves are under pressure, why a supplier payment in euros cost significantly more than budgeted, and why the liquidity position that looked comfortable in January has tightened considerably by April. None of this happened because the business performed poorly. It happened because the financial infrastructure did not keep pace with the complexity of the operation. Effective treasury management UAE is not a back-office function that matters only when something goes wrong.it is the discipline that determines whether a multinational firm’s commercial success actually translates into financial stability. This guide addresses currency risk, liquidity planning, and the practical decisions that separate firms that grow sustainably from those that grow fast and then scramble.

Why Global Growth Creates Financial Complexity?

The relationship between international expansion and financial risk is not linear. Every new market a Dubai firm enters introduces a new currency to manage, a new supplier payment cycle to fund, and a new set of timing mismatches between revenue and cost. A company operating across five markets with revenues in four different currencies and procurement in three others is managing a financial structure that looks nothing like its domestic counterpart yet many of these firms apply the same treasury thinking they used when they operated in a single currency.

The result is delayed visibility. By the time consolidated financial reports capture a currency-driven margin compression, the damage is already done. By the time a cash shortfall becomes visible at headquarters, the subsidiary has been managing it with short-term borrowing for weeks. Fragmented reporting and decentralised decision-making are not just inefficiencies; they are risk multipliers in a multinational structure.

The Silent Threat to Profitability(Currency Risk)

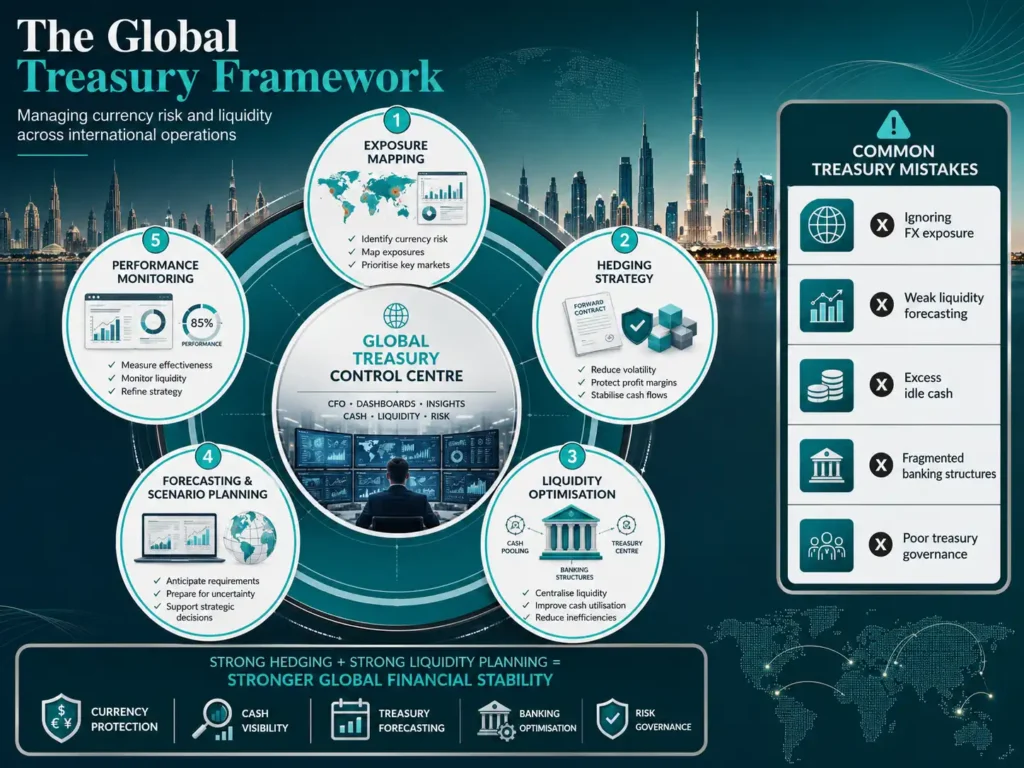

Currency exposure takes three distinct forms, and most firms manage only the most visible one.

Transaction exposure covers the risk on specific future cash flows denominated in euros, payable due in sterling, a contract priced in dollars. This is the exposure most treasury teams think about because it is concrete and measurable.

Translation exposure is subtler. When a Dubai firm consolidates the accounts of a European subsidiary into AED-denominated group financials, exchange rate movements between reporting dates change the reported value of those assets and liabilities without a single transaction having occurred. For firms with significant overseas operations, this can produce meaningful swings in reported financial position.

Economic exposure is the longest-term and most easily ignored. A firm that competes with European manufacturers in a third market is affected by EUR movements even if it has no euro transactions because its competitor’s cost structure changes relative to its own when currencies shift.

The AED-USD Peg Does Not Mean Zero FX Risk

This is where many Dubai multinationals make a significant error. The AED’s peg to the US dollar provides genuine stability in dollar-denominated transactions, but the majority of global trade does not happen exclusively in dollars. A firm importing from Germany, selling to UK clients, sourcing from India, and paying a logistics provider in China manages euro, sterling, rupee, and yuan exposure regardless of the AED peg.

Consider a practical scenario: a Dubai distributor sources products from Italy priced in euros, sells to Gulf clients in AED, and reports in AED. When the euro strengthens against the dollar by eight percent over a quarter, the cost of goods purchased from Italy rises by the same proportion, while revenues in AED remain flat. The margin compression is real, immediate, and entirely invisible to any analysis that starts and ends with AED-USD.

The Profitability vs Liquidity Trap

Profitability and liquidity are related but not identical, and confusing the two is one of the more costly mistakes a growing business can make.

Revenue recognition and cash collection are separated by payment terms. A multinational firm with 90-day collection terms on its largest clients may be recognising revenue every month while waiting three months for the cash to arrive. Meanwhile, supplier obligations, payroll across multiple jurisdictions, and lease commitments fall due continuously. The working capital gap this creates is a structural feature of the business model, not a temporary cash flow blip.

Rapid expansion makes this significantly worse. Opening a new regional office requires cash before it generates revenue. Winning a large contract requires inventory procurement before the client pays anything. Hiring ahead of growth which most firms must do creates fixed cost commitments that precede the revenue they are intended to support. The warning signs are predictable: receivables growing faster than revenue, cash reserves declining despite profitability, increasing reliance on short-term credit lines to cover operational commitments that should be funded from trading cash flow.

Liquidity Planning: Building Financial Stability

Liquidity planning is not the same as cash flow forecasting, though forecasting is its most important component. True liquidity planning integrates three time horizons simultaneously.

Short-term forecasting, typically thirteen weeks rolling, provides the operational visibility to manage payment timing, identify upcoming shortfalls early, and avoid the last-minute scrambles that force bad decisions. Medium-term forecasting, covering six to eighteen months, supports working capital decisions, investment timing, and financing needs. Long-term liquidity planning connects treasury to the corporate strategy ensuring that the financial infrastructure can support growth plans rather than discovering, mid-execution, that it cannot.

The question of liquidity buffer how much cash to hold in reserve is one every CFO wrestles with. Too little creates vulnerability to shocks. Too much represents an opportunity cost, particularly for firms with good investment alternatives. The practical answer depends on cash flow volatility, client payment behaviour, and the availability of committed credit facilities as a backstop. A reasonable starting point for most Dubai multinationals is six to eight weeks of fixed operating costs, held in a form that is genuinely accessible rather than technically available but operationally trapped.

How Multinationals Manage Currency Risk in Practice?

Hedging Instruments

Forward contracts are the most commonly used hedging tool for a straightforward reason: they eliminate uncertainty on a specific cash flow at a specific date. A Dubai firm expecting to pay a European supplier in euros in ninety days locks in today’s rate, removing the risk of adverse movement between now and then. The limitation is rigidity,if the underlying transaction changes, the hedge creates its own exposure.

Currency options provide the right but not the obligation to transact at a specified rate. They cost more than forwards; the premium is the price of optionality but they preserve the ability to benefit from favourable movements. Options suit situations where the underlying cash flow is uncertain in timing or amount.

Currency swaps exchange principal and interest obligations in one currency for equivalent obligations in another, typically used for longer-dated exposures or funding structures with currency mismatches.

Natural hedging deserves more attention than it typically receives. A firm that can match revenue and cost in the same currency eliminates the FX exposure at source rather than managing it with derivatives. Sourcing locally in a market where revenue is earned, or pricing contracts in the currency of the cost base, reduces the hedging requirement without any financial instrument.

How Much to Hedge?

There is no universally correct hedge ratio, and firms that believe otherwise tend to create as many problems as they solve. The decision depends on the firm’s risk tolerance, the stability of its cash flow forecasts, the characteristics of the currencies involved, and the cost of hedging relative to the exposure.

The most common mistake is over-hedging based on optimistic revenue forecasts. A firm that hedges 100 percent of projected euro revenues and then collects only 70 percent of that forecast has a hedge position that exceeds its actual exposure creating a speculative position rather than a risk management one. Layered hedging, hedging a portion of forecast exposure at each planning horizon and adding coverage as certainty increases avoids this problem while providing meaningful protection against adverse movements.

Centralising Cash Across Global Operations

One of the most persistent challenges for Dubai multinationals is trapped cash funds sitting in subsidiary accounts in markets where they cannot easily be repatriated or deployed elsewhere. A firm with AED 50 million in total group cash but AED 30 million of that concentrated in markets with capital controls or repatriation restrictions does not have AED 50 million of accessible liquidity.

Cash pooling structures address this by consolidating balances across multiple accounts notionally or physically so that surplus cash in one entity offsets deficits in another without requiring the individual entities to borrow externally. Centralised treasury structures take this further, with a single treasury function managing group-wide liquidity, FX risk, and banking relationships rather than leaving each subsidiary to manage independently.

The practical benefit is visibility. A centralised structure gives the CFO a real-time view of where cash sits, where it is needed, and where excess liquidity can be deployed most efficiently. The decentralised alternative produces a patchwork of subsidiary balances that take weeks to consolidate and describe positions that are already outdated by the time they arrive.

Treasury’s Role in International Expansion

Growth decisions and treasury decisions are not independent. A CFO who learns about a planned acquisition or market entry after the term sheet is signed has lost the ability to structure the transaction in a treasury-efficient way. Working capital requirements in the new market, the currency of the funding, the tax implications of the intercompany structure all of these are treasury questions that benefit from being answered before the commercial decision is finalised rather than after.

Firms with mature treasury management UAE practices bring treasury into strategic decisions early. The result is not that treasury slows down growth.it is that the growth that happens is funded in a way that does not create the liquidity pressures that otherwise arrive as unwelcome surprises twelve months later.

Treasury Metrics That Matter

Six metrics provide the core visibility a multinational treasury function needs.

The cash conversion cycle measures how long cash is tied up between paying for inputs and collecting from customers. Lower is better, and a lengthening trend signals working capital deterioration before it becomes a cash crisis. Days Sales Outstanding and Days Payable Outstanding measure the receivables and payables components of that cycle respectively, and monitoring both separately identifies where the pressure is concentrated.

Liquidity coverage comparing available liquid assets to short-term obligations gives a sense of buffer adequacy. Forecast accuracy, measured by comparing actual cash positions to what was forecast four to eight weeks earlier, tells a treasury team whether its planning process is working or producing comfortable-looking numbers that bear little relationship to reality. Cash flow at risk, a more sophisticated measure, quantifies the potential downside on cash positions under adverse scenarios.

Preparing for Uncertainty

Scenario planning is where treasury discipline becomes most visible in a crisis. A firm that has modelled a thirty percent revenue decline, a three-month payment delay from its largest client, and a fifteen percent adverse currency movement before any of those things happen has a response framework ready. A firm that encounters the same scenarios without preparation makes decisions under pressure with less information and fewer options.

Liquidity stress testing is the practical implementation of scenario planning testing whether the firm’s liquidity position survives a defined set of adverse conditions and identifying in advance what actions would be required if it did not. Contingency funding plans, pre-arranged credit facilities, asset disposal plans, intercompany funding mechanisms convert the scenario analysis from an academic exercise into an operational capability.

Frequently Asked Questions

A Dubai firm invoices clients in AED but sources from Europe does it still carry currency risk?

Yes. The AED-USD peg covers dollar transactions but offers no protection against euro or sterling movements. When a firm buys in euros and sells in AED, every EUR-USD movement directly affects procurement costs while revenues remain unchanged. The margin compression is real and often goes unnoticed until quarterly figures reveal a profitability gap nobody can easily explain.

What is the practical difference between a forward contract and a currency option?

A forward locks in an exchange rate for a future transaction certainty in both directions, no premium, but no ability to benefit if rates move favourably. An option buys the right to transact at a specified rate without the obligation, preserving upside but costing a premium. Forwards suit confirmed payables and receivables. Options suit situations where transaction timing or amount remains uncertain.

How does a Dubai multinational avoid over-hedging its currency exposure?

By hedging forecast exposure in layers rather than covering the full projected position at once. A firm hedging one hundred percent of projected revenues and then collecting only seventy percent has created a speculative position; the hedge now exceeds actual exposure. Building coverage progressively as cash flows become more certain avoids this while still providing meaningful protection.

What is cash pooling and when does it make sense?

Cash pooling consolidates balances across subsidiary accounts so surplus cash in one entity offsets deficits in another, avoiding external borrowing while idle cash sits elsewhere. It makes practical sense once a group operates across three or more jurisdictions with regular intercompany cash movement. The main barriers are regulatory; some markets restrict repatriation or intercompany lending in ways that limit pooling structures.

How frequently should a Dubai multinational update its liquidity forecast?

Short-term forecasts covering thirteen weeks should be updated weekly. Medium-term forecasts covering six to eighteen months should be refreshed monthly. What matters most is consistently comparing forecasts to actual a treasury team that never measures its accuracy has no way of knowing whether its planning process is reliable or simply producing optimistic numbers that create a false sense of control.

Conclusion

Currency risk and liquidity management are two dimensions of the same challenge: ensuring a business’s financial position reflects its commercial performance rather than being quietly undermined by timing gaps, FX movements, and visibility failures.

Dubai Business and Tax Advisors works with Dubai-based multinationals to build that discipline from currency exposure assessments and hedging strategy to liquidity forecasting and cash pooling so finance teams stay ahead of risk rather than reacting to it.

The firms that discover treasury’s importance only when something goes wrong have already paid a significant portion of the tuition fee. Dubai Business and Tax Advisors is here to make sure that cost is never necessary.